The landscape of hematology-oncology treatment has undergone significant transformations recently with the entry of new therapeutic drugs. As new treatment options become available, market dynamics shift. Tracking the impacts of these entries is important to both inform Life Sciences strategies and understand the dynamics of therapeutic competition, shifts in clinical practice, and changes in patient access to cutting-edge treatments.

We sought to track market share adaptation in the use of five hematologic oncology drugs: BRUKINSA®, IMBRUVICA®, VENCLEXTA®, ICLUSIG®, and CALQUENCE®. These drugs entered the market between 2018 and 2023 and are captured with high visibility in Komodo’s Healthcare Map™, which offers unique coverage of the hematology-oncology space. We used National Drug Codes and relevant procedure codes and also looked for relevant demographic variations. We used data from Komodo Health’s MapLab™ and MapView™ solutions to analyze and visualize medical and pharmacy claims from 2016 through 2023. Here’s what we found:

Market Adoption

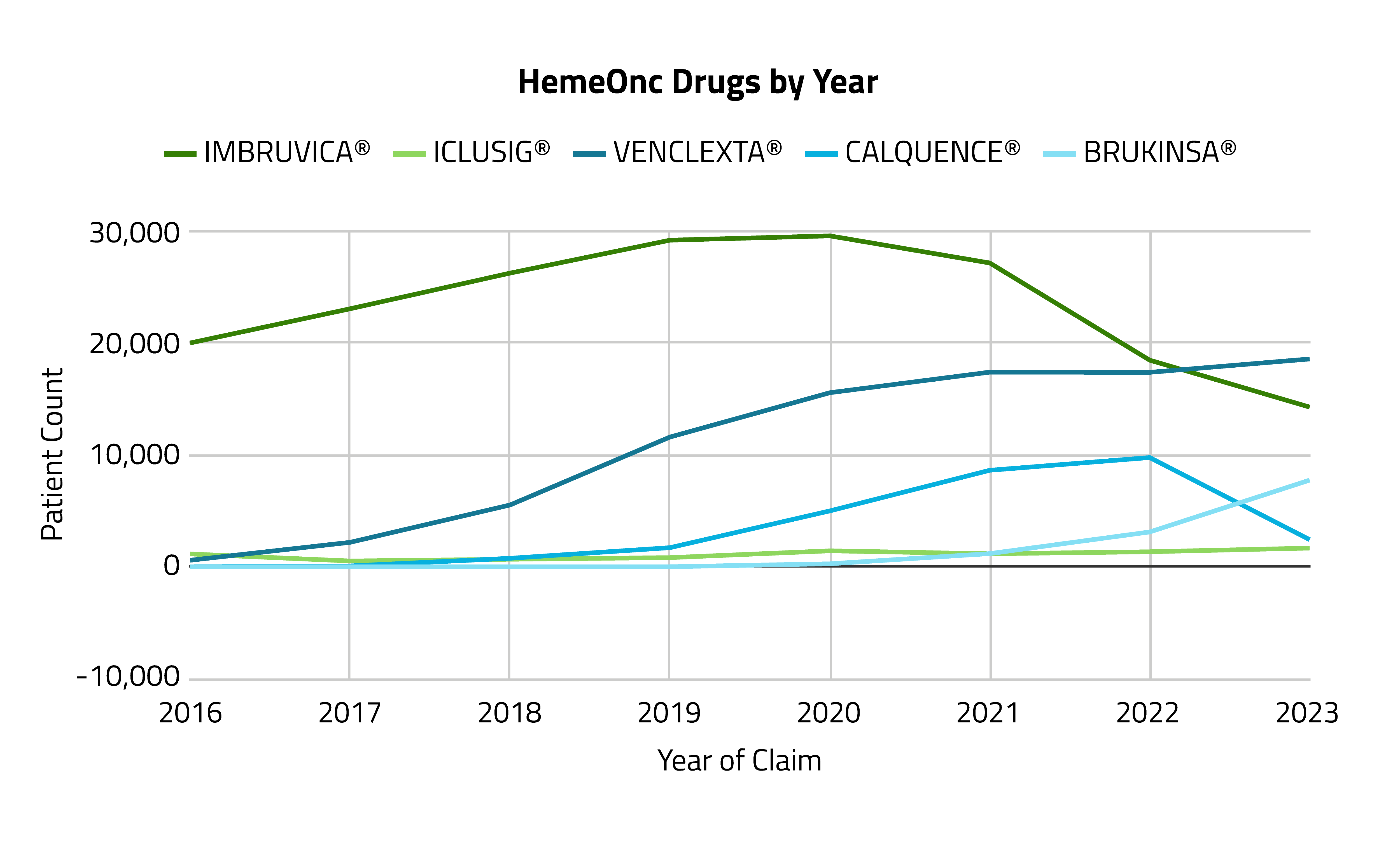

- We found a significant decline in the dominance of IMBRUVICA® in the years leading up to 2023 as new drugs entered the market. BRUKINSA®, which was approved for chronic lymphocytic leukemia by the FDA in January 2023, demonstrated a remarkable growth of 149% from 2022 to 2023. Conversely, IMBRUVICA® patient counts decreased by 51% from a peak in 2019.

- By 2023, VENCLEXTA® emerged as the leading therapeutic among the five, claiming 42% of the market basket share. The rapid ascent of BRUKINSA® and the decline of IMBRUVICA® illustrate the competitive nature of the market and potentially shifting clinical preferences.

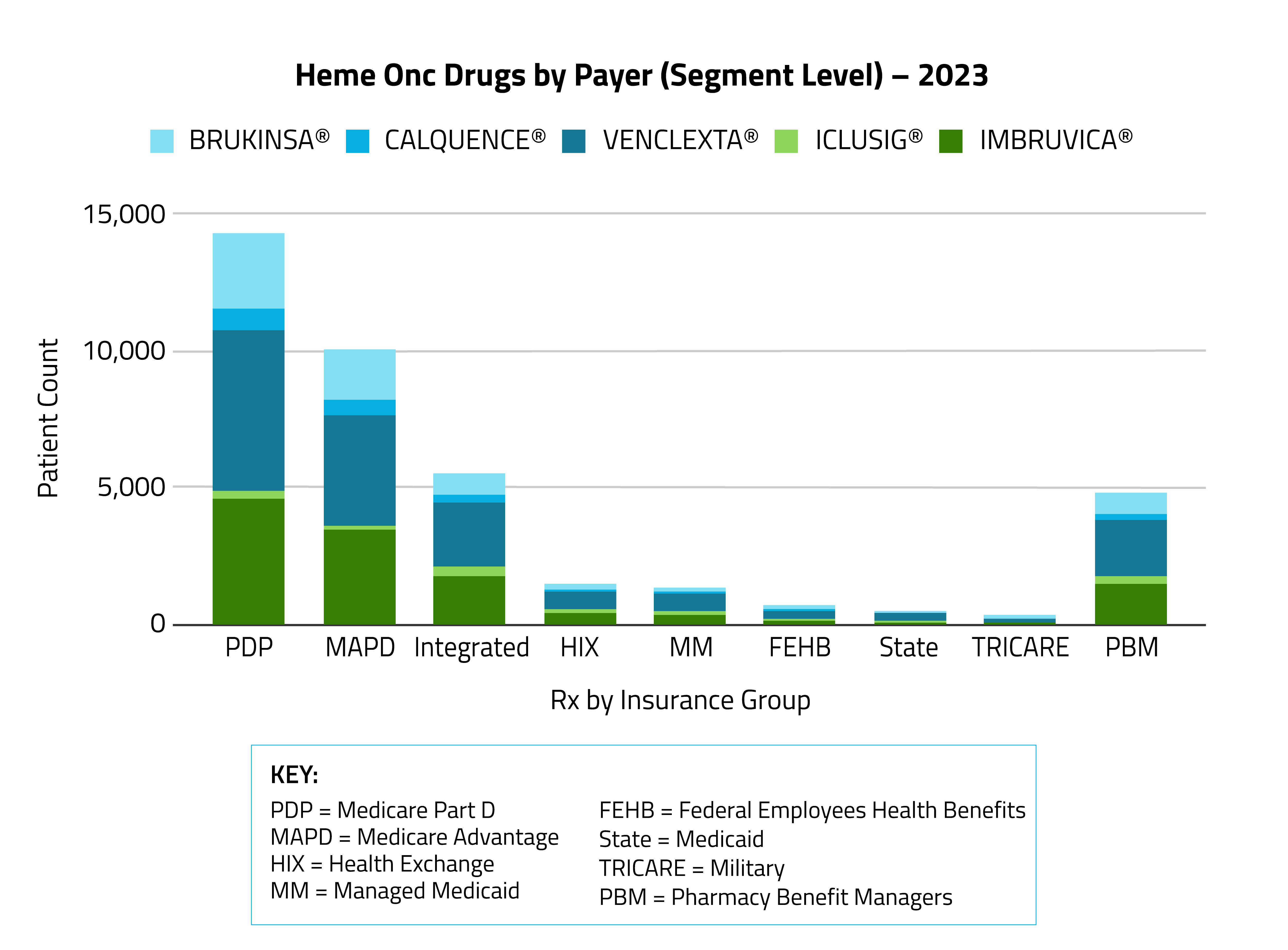

Payers and Demographics

- Medicare was found to be the dominant payer across most prescriptions.

Race and Ethnicity

- Non-Hispanic Whites made up the largest percentage of the treated population, at 76% — significantly greater than their 58% representation in the U.S. population.

- Treated patients were also more likely to be male, at 61%.

These demographic findings align with existing literature that shows higher incidence rates among White patients and male patients for the most common blood cancers: leukemia and non-Hodgkin lymphoma.

This high-fidelity tracking of new therapeutic entries to the market provides crucial insights for healthcare providers, policymakers, and researchers as they work to optimize treatment strategies and address equity in healthcare access. By leveraging detailed, real-time insights, Life Sciences organizations can refine market positioning, adjust marketing tactics, and tailor patient outreach to align with healthcare provider preferences and patient needs. The strategic use of tools that offer in-depth visibility and healthcare analytics can enhance drug adoption and optimize patient care while maintaining competitiveness in the fast-evolving oncology sector and working toward the shared goal of reducing the burden of disease.

To see more articles like this, follow Komodo Health on X, LinkedIn, or YouTube, and visit Insights on our website.